Buying your first home in New Zealand is a huge milestone — and also one of the most financially significant decisions you’ll make. Whether you’re dreaming about owning a home or already attending open homes, the mortgage journey can feel overwhelming without a clear roadmap. In 2025, interest rate fluctuations, tighter lending rules, and government incentives have made it even more important to understand the process thoroughly.

So let’s break down the stages that first-home buyers go through, alongside their mortgage advisor, from the moment they start thinking about buying a home right through to settlement and moving in.

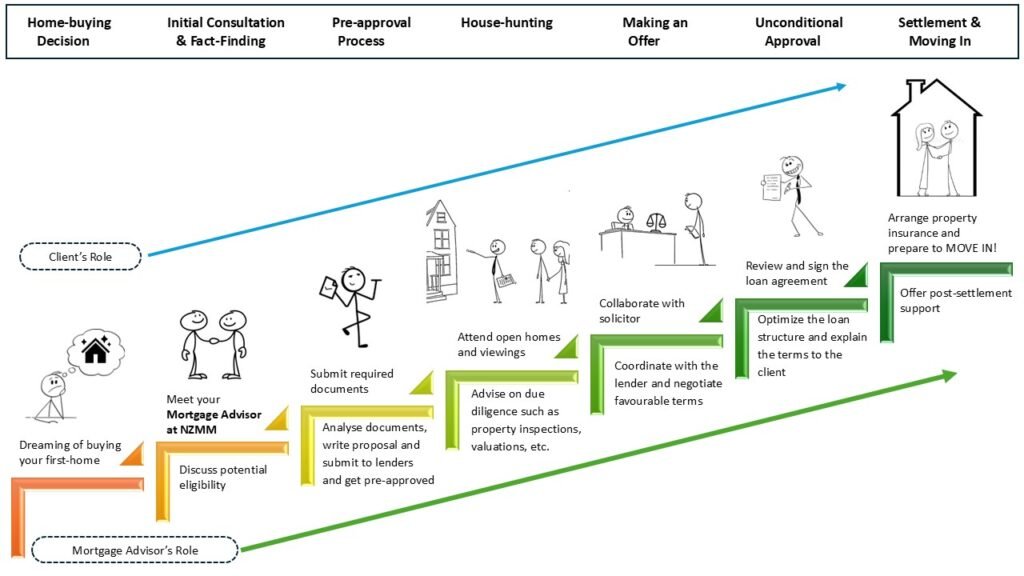

Home-buying process broken down to 7 steps

Home buying can be broken down to a 7 steps process. The journey begins with a dream and determining if you are ready to buy a home. Most first-time buyers start by browsing listings online, using mortgage calculators, and reading up on how much they might be able to borrow. At this early stage, it’s natural to feel unsure about where to begin.

“The good news is, with a mortgage advisor, you can ensure that every step you take leads to success!”

This is where we, as mortgage advisors at NZ Mobile Mortgages (NZMM), can offer immense value by educating our clients to help them understand what’s ahead. According to the Financial Markets Authority, many people still don’t realise the advantages of seeking early advice, which can save thousands over the life of a loan.

Next comes the initial consultation — a more formal and focused phase of the process. Here, the prospective buyer will have a detailed discussion with the mortgage advisor, to discuss their financial position, including income, savings, expenses, and debts. This is often an eye-opening stage for the buyer, as the advisor will help determine how much the client can reasonably borrow and what loan structures might suit their goals. For many, it’s also the first time they learn about assistance programs like KiwiSaver withdrawals or Kainga Ora’s First Home Loan, which allow eligible buyers to secure a home loan NZ with just a 5% deposit.

“We do the heavy lifting so you can focus on the exciting part — finding your dream home.”

Once financial readiness is confirmed, the advisor helps the client prepare for pre-approval. This stage involves collecting important documentation like ID, pay slips, and bank statements. With these, the advisor submits an application to one or more lenders. According to ANZ Bank, getting a pre-approval — essentially a conditional offer of finance — gives buyers a clear idea of what they can afford and strengthens their position when they’re ready to make an offer. Pre-approvals are important in competitive markets and can take time, so early preparation is key.

With the pre-approval in hand, the buyer can now move into the house-hunting phase. This is often the most exciting part — but also the most time-consuming. Buyers attend open homes, research local markets, and narrow down their ideal home based on affordability and lifestyle. During this phase, advisors remain in the loop, offering guidance on whether a property is realistically within budget, and providing contacts for building inspectors, real estate agents, or property lawyers. They can also advise on due diligence, such as checking the LIM report and understanding auction procedures.

“Our trusted network of home-loan service providers ensures you have access to top-tier expertise and deals!”

Once a suitable property is found, the buyer makes an offer. This can be either conditional (subject to finance, building report, etc.) or unconditional, depending on their confidence and the competition in the market. A mortgage advisor works closely with both the client and their solicitor to ensure the offer aligns with lender expectations and that any conditions will be manageable. They’ll also work closely with the lender to secure final approval, making sure the property meets the bank’s lending criteria. As ASB bank correctly stated, a mortgage advisor takes the hassle out of the process by liaising with the bank.

After the offer is accepted, and conditions are met, the buyer enters the formal approval and documentation stage. This is when the loan is locked in and the buyer signs official mortgage documents. The advisor will review the loan structure with the client — discussing fixed versus floating rates, repayment types, and possible future reviews. This stage is critical in ensuring the client doesn’t just get a loan, but gets the right loan for their lifestyle and long-term goals.

Finally, the journey concludes with settlement and moving in. The buyer arranges insurance, prepares to pay final costs, and waits for the exciting moment when the keys are handed over. The advisor coordinates closely with lawyers and banks to ensure the funds are released on time and that settlement proceeds smoothly. Even after the buyer moves in, a good advisor stays in touch for ongoing reviews, helping clients consider refinancing options or financial restructuring in the future.

Throughout all these stages, the support of a professional mortgage advisor is invaluable. Not only can they save clients from common mistakes, but they also offer access to a broader range of lenders and products than a single bank can. They advocate on behalf of the buyer, streamline paperwork, and provide clarity in what can be an emotionally intense process.

“Let us navigate the paperwork & numbers — so you can enjoy the keys to your future.”

As a first-time buyer, understanding this journey empowers you to plan ahead and approach each step with confidence. Are you ready to take the first step toward your dream home? Get in touch today for personalised mortgage advice to start your journey with confidence. NZ Mobile Mortgages team is committed to helping you stay on track and feel fully prepared throughout your mortgage journey.